Making sound lending and investment decisions is the cornerstone of financial stability. Whether you are a bank, a credit union, or a business extending credit to customers, the ability to accurately assess creditworthiness is paramount. A standardized and comprehensive Credit Analysis Report Template is an indispensable tool in this process, providing a structured framework to evaluate a borrower’s ability and willingness to repay debt. This structured approach moves credit assessment from a subjective gut feeling to an objective, data-driven analysis, ensuring consistency and minimizing the risk of costly defaults.

A Credit Analysis Report, often abbreviated as CAR, is a detailed document that synthesizes quantitative and qualitative data to paint a complete picture of a potential borrower’s financial health. It scrutinizes financial statements, evaluates management capabilities, and considers the broader economic environment. Without a consistent template, analysts might overlook critical risk factors, leading to inconsistent evaluations across different loan applications. This can result in approving risky loans or rejecting creditworthy applicants, both of which negatively impact an organization’s bottom line.

By implementing a well-designed template, financial institutions and businesses can streamline their credit review process significantly. It ensures that all necessary components are considered for every application, from basic borrower information to complex financial ratio analysis. This not only enhances efficiency and reduces turnaround times but also serves as an excellent training guide for junior analysts and a reliable reference for audit and compliance purposes. This article will delve into the essential components of a robust credit analysis report, explain why a template is a strategic asset, and guide you on how to build one tailored to your specific needs.

What is a Credit Analysis Report?

A Credit Analysis Report (CAR) is an in-depth assessment prepared by a credit analyst to determine the creditworthiness of an individual or, more commonly, a business entity. Its primary purpose is to evaluate the risk associated with extending credit or a loan to that entity. The report serves as a foundational document for decision-makers, such as loan officers, credit committees, and investment managers, providing a clear recommendation to approve, deny, or modify a credit request.

The core function of a CAR is to answer one fundamental question: What is the likelihood that the borrower will be able to meet their debt obligations on time and in full? To answer this, the report synthesizes a wide range of information. It goes beyond simply looking at a credit score. It involves a meticulous examination of financial history, current financial position, and future projections. The analysis covers both the quantitative aspects, such as revenue trends and debt levels, and qualitative factors, like the strength of the management team and the company’s position within its industry.

Ultimately, the report culminates in a risk rating and a recommendation. This is not just a simple “yes” or “no.” It often includes specifics on the proposed credit facility, such as the loan amount, interest rate, repayment term, and required covenants. These covenants are conditions or restrictions placed on the borrower to protect the lender’s interests throughout the life of the loan. A well-prepared CAR provides the clarity and evidence needed to structure a credit deal that balances the borrower’s needs with the lender’s risk appetite.

The Core Components of a Credit Analysis Report Template

A comprehensive template is built upon a logical structure that guides the analyst through a systematic evaluation. While the level of detail may vary depending on the complexity of the credit request, a robust template will almost always include the following core sections.

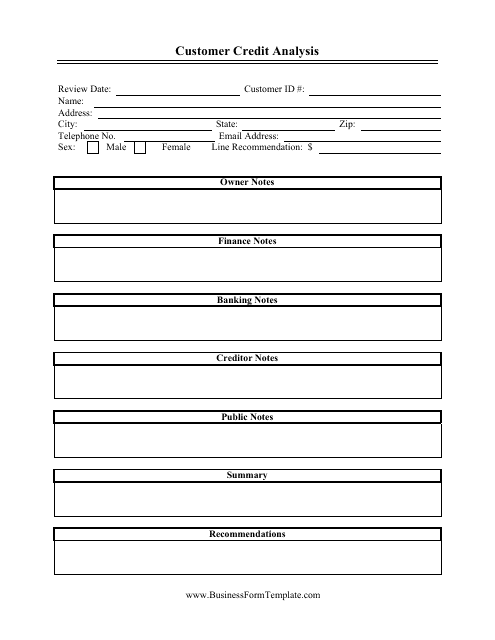

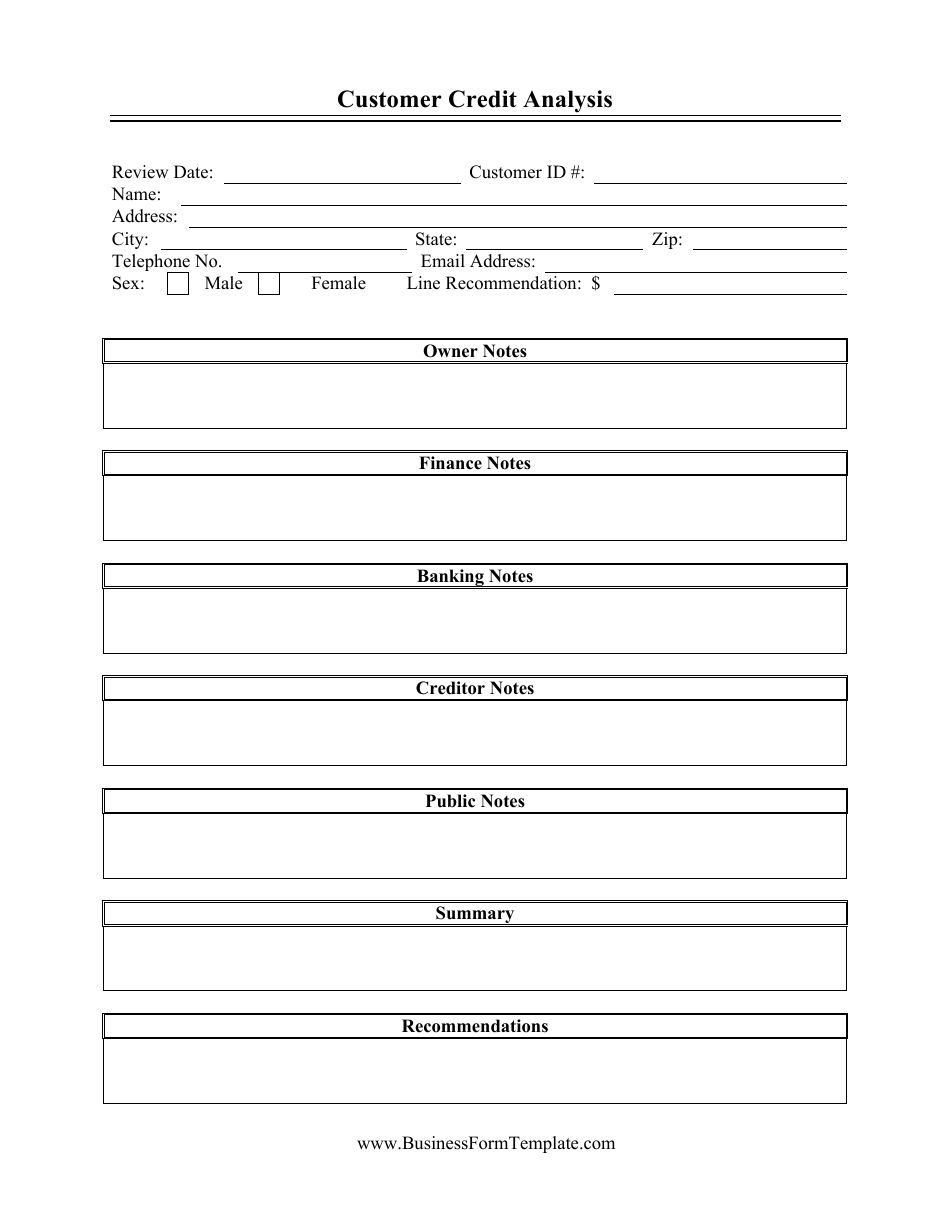

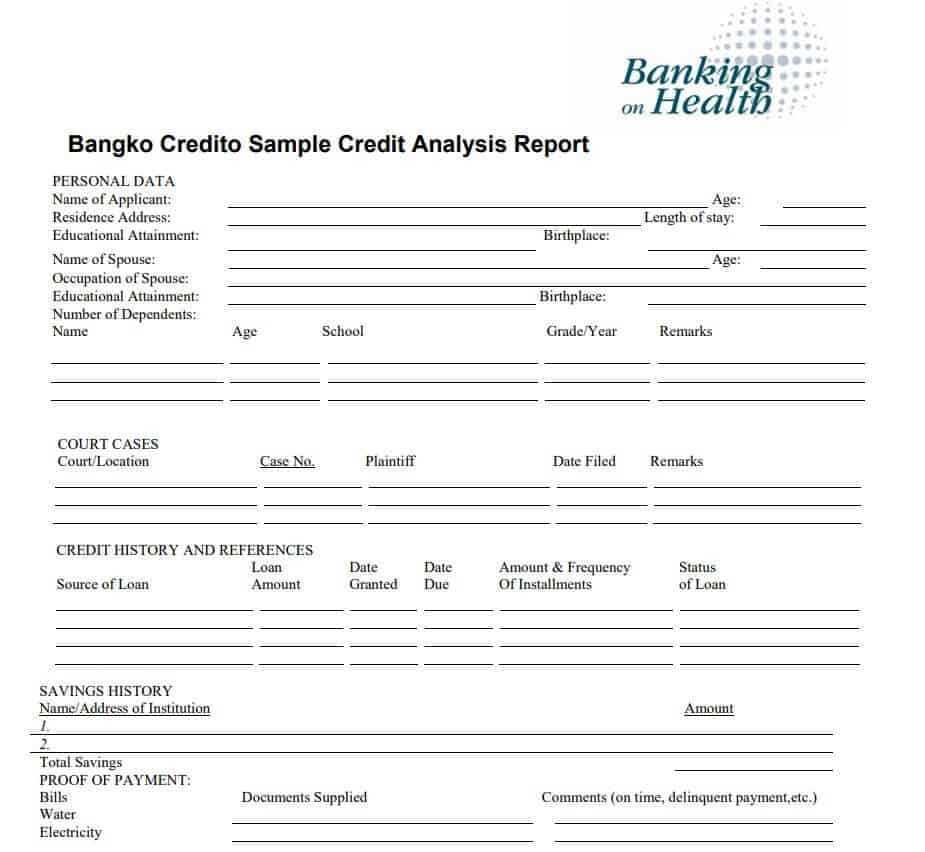

Borrower and Request Information

This initial section sets the stage for the entire report. It provides a snapshot of who the borrower is and what they are asking for.

- Borrower Details: This includes the legal name of the business, address, legal structure (e.g., Corporation, LLC, Sole Proprietorship), date of establishment, and primary contact information.

- Loan Request: Clearly state the purpose of the loan (e.g., working capital, equipment purchase, real estate acquisition), the amount requested, and the proposed repayment term.

- Business & Industry Overview: A brief description of the business’s operations, its products or services, and an overview of the industry in which it operates.

The 5 Cs of Credit: A Foundational Framework

The 5 Cs of Credit is a time-tested methodology used by lenders worldwide to gauge the creditworthiness of potential borrowers. Your template should have a dedicated section for analyzing each “C.”

- Character: This refers to the borrower’s reputation and track record of repaying debts. It’s an assessment of integrity. The analysis here includes reviewing credit reports, checking for past defaults or bankruptcies, and evaluating the experience and reputation of the management team.

- Capacity: This is a quantitative measure of the borrower’s ability to repay the loan from its operating cash flow. Key metrics include the Debt Service Coverage Ratio (DSCR), which compares cash available to the required debt payments. A ratio above 1.25x is often considered healthy.

- Capital: This assesses the borrower’s own financial investment in the business. It indicates how much the owner has at risk. Lenders look at the company’s net worth and its debt-to-equity ratio. A high level of owner equity provides a cushion against losses and demonstrates a commitment to the business.

- Collateral: These are the assets the borrower pledges as security for the loan. If the borrower defaults, the lender can seize the collateral to recoup its losses. The report should detail the type of collateral (e.g., real estate, accounts receivable, inventory), its estimated value, and its liquidity.

- Conditions: This refers to the external factors that could impact the borrower’s ability to repay, such as the state of the economy, industry trends, and the competitive landscape. A thorough analysis considers how these macro-level conditions might affect the business’s future performance.

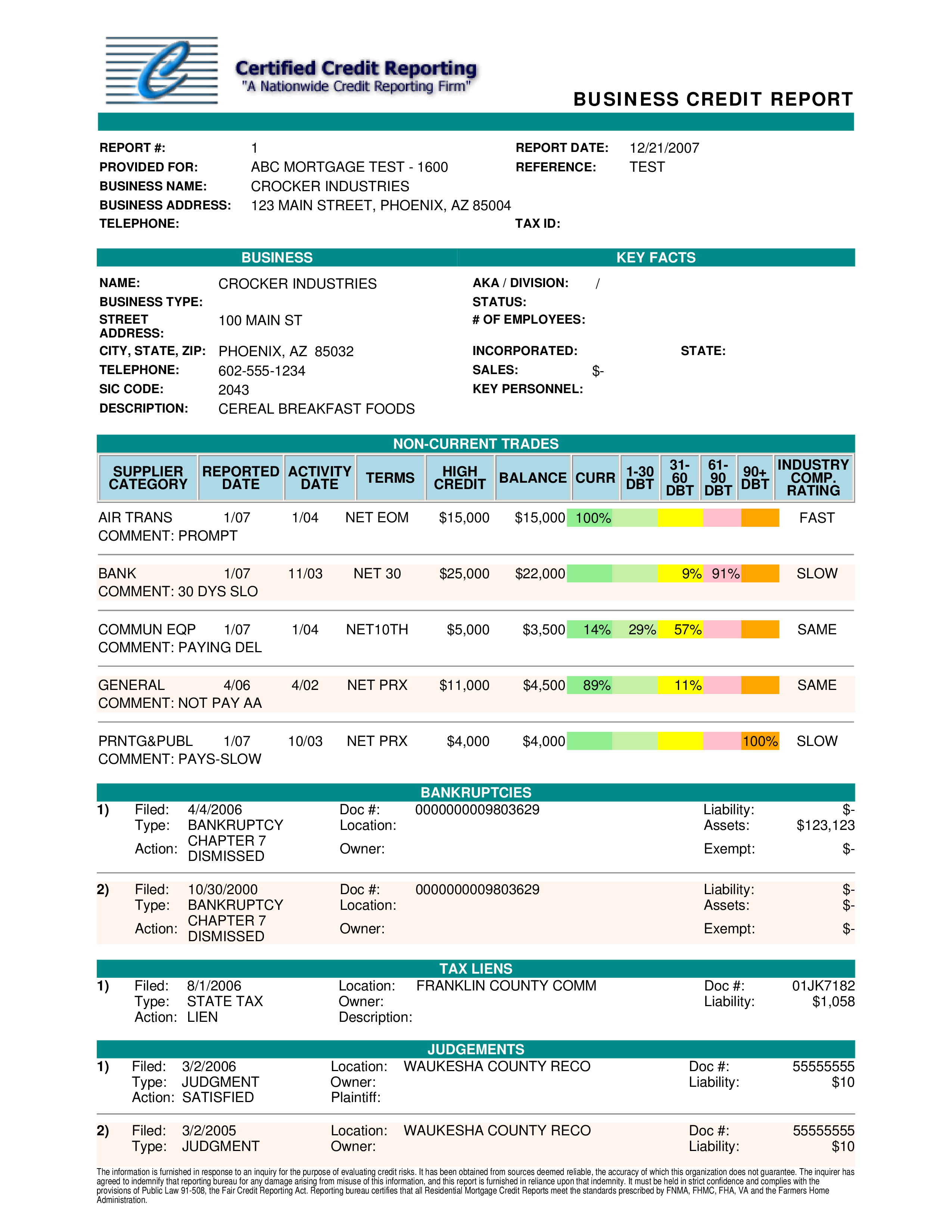

Financial Statement Analysis

This is the heart of the quantitative analysis. The template should include sections for spreading and analyzing at least three years of historical financial statements, plus interim statements if available.

- Income Statement: Analyze revenue trends, gross profit margins, operating expenses, and net profitability. Look for consistency, growth, and the ability to control costs.

- Balance Sheet: Evaluate the company’s assets, liabilities, and equity. Key areas of focus include the quality of assets (e.g., age of accounts receivable), the structure of liabilities (short-term vs. long-term debt), and the overall solvency of the business.

- Cash Flow Statement: This is arguably the most critical statement as it shows where the company’s cash is coming from and where it is going. Analyze cash flow from operations, investing, and financing to understand the company’s ability to generate cash internally.

Key Financial Ratio Analysis

Your template should automate the calculation of key financial ratios to allow for quick comparison over time and against industry benchmarks.

- Liquidity Ratios: Measures the ability to meet short-term obligations. Examples include the Current Ratio and Quick Ratio.

- Leverage Ratios: Indicates the extent to which a company relies on debt. Examples include the Debt-to-Equity Ratio and Total Debt-to-Assets.

- Profitability Ratios: Shows how effectively the company is generating profits from its sales and assets. Examples include Net Profit Margin and Return on Equity (ROE).

- Efficiency Ratios: Evaluates how well a company is using its assets and liabilities. Examples include Inventory Turnover and Days Sales Outstanding (DSO).

Summary and Recommendation

The final section synthesizes all the findings into a coherent conclusion.

- Strengths & Weaknesses: A bulleted list summarizing the key positive and negative factors identified during the analysis.

- Risk Assessment: An overall assessment of the credit risk, often assigned a numerical or letter grade.

- Recommendation: A clear recommendation to approve, decline, or modify the loan request, including the proposed loan structure, interest rate, term, and any necessary covenants.

Why a Standardized Template is a Strategic Advantage

Adopting a standard template for credit analysis is more than just a matter of convenience; it is a strategic decision that enhances risk management and operational efficiency.

Ensures Consistency and Objectivity

Without a template, two different analysts might evaluate the same loan application and arrive at vastly different conclusions based on their individual methods and biases. A Credit Analysis Report Template enforces a uniform methodology, ensuring that every application is subjected to the same level of scrutiny. This consistency is crucial for fair lending practices and for building a reliable historical database of credit decisions.

Increases Efficiency and Productivity

Credit analysis is a time-intensive process. A template provides a clear roadmap, guiding the analyst through each step and eliminating the need to build a report from scratch every time. Pre-built sections, automated ratio calculations in spreadsheet-based templates, and standardized formatting allow analysts to focus their energy on critical thinking and interpretation rather than on administrative tasks. This leads to faster turnaround times on loan applications, improving customer satisfaction.

Mitigates Risk of Omission

In a complex analysis, it is easy to overlook a critical piece of information. A well-designed template acts as a checklist, ensuring that all key risk areas—from financial ratios to qualitative management assessment—are thoroughly investigated. This systematic approach significantly reduces the risk of making a credit decision based on incomplete information, thereby protecting the lender from potential losses.

Facilitates Training and Auditing

For financial institutions, a standardized template is an invaluable training tool for new or junior credit analysts. It provides them with a structured framework that embodies the organization’s credit philosophy and analytical standards. Furthermore, during internal or external audits, having consistent and well-documented reports makes the review process smoother and more transparent, demonstrating a commitment to sound risk management practices.

How to Build Your Own Credit Analysis Report Template

Creating a custom template allows you to tailor the analysis process to your specific industry, risk tolerance, and business needs. Here is a step-by-step guide to building an effective template.

Step 1: Define Your Purpose and Scope

Start by clarifying the primary use of the template. Are you evaluating large corporate loans, small business credit lines, or trade credit for customers? The complexity and focus of your template will differ for each. A template for a $5 million commercial real estate loan will require far more detail on collateral and cash flow projections than one for a $10,000 trade credit line.

Step 2: Outline the Key Sections

Using the core components discussed earlier as a guide, map out the structure of your report. Start with high-level sections (##) like “Borrower Information,” “Financial Analysis,” and “Recommendation.” Then, break these down into more granular sub-sections (###) such as “Liquidity Ratios,” “SWOT Analysis,” and “Proposed Covenants.”

Step 3: Choose the Right Format

The most common formats for credit analysis templates are spreadsheets (like Microsoft Excel or Google Sheets) and word processors (like Microsoft Word).

- Spreadsheets: Highly recommended for their ability to handle financial data. You can create separate tabs for financial statement inputs, ratio calculations, and the final report. The ability to automate calculations with formulas is a major advantage.

- Word Processors: Better suited for reports that are more narrative-heavy. However, they lack the computational power of spreadsheets, meaning financial data must be calculated and imported separately.

A hybrid approach is often best, where the quantitative analysis is done in a spreadsheet and the final, polished report with narrative and charts is compiled in a word processor.

Step 4: Develop the Content and Formulas

Flesh out each section with the specific fields, tables, and prompts required. For a spreadsheet template, this is where you build the formulas to automatically calculate financial ratios, trends, and debt service coverage. For example, the cell for the Current Ratio should contain a formula like = (Total Current Assets) / (Total Current Liabilities). Include clear instructions or prompts to guide the user on what information to enter and how to interpret the results.

Step 5: Test and Refine the Template

Before rolling out the template for general use, test it with several past or current loan applications. This “beta testing” phase is crucial for identifying any issues, such as broken formulas, unclear sections, or missing data points. Get feedback from experienced analysts and incorporate their suggestions to make the template more robust and user-friendly.

Common Pitfalls to Avoid in Credit Analysis

Even with a great template, analysts can fall into common traps that compromise the quality of their assessment. Being aware of these pitfalls is essential for maintaining objectivity and accuracy.

Over-Reliance on Historical Data

While historical financial performance is a critical indicator, it is not a guarantee of future results. A business that was highly profitable in the past may be facing new competition or disruptive technologies. A thorough analysis must include forward-looking elements, such as reasonable financial projections and a consideration of industry trends.

Ignoring Qualitative Factors

Numbers alone do not tell the whole story. An analyst who focuses solely on financial ratios might miss critical risks related to a weak management team, a high concentration of customers, or a poor succession plan. The qualitative analysis of management, industry, and competitive positioning is just as important as the quantitative analysis.

Confirmation Bias

Confirmation bias is the tendency to search for, interpret, and favor information that confirms one’s pre-existing beliefs. An analyst who has an initial positive feeling about a borrower might subconsciously downplay negative information. To combat this, analysts must actively seek out disconfirming evidence and play the role of a skeptic, challenging assumptions throughout the process.

Lack of Industry-Specific Knowledge

Analyzing a software company using the same metrics as a manufacturing company can be misleading. Different industries have different business cycles, capital requirements, and key performance indicators. A skilled analyst understands the unique dynamics of the borrower’s industry and uses relevant benchmarks for comparison.

Conclusion

A well-structured Credit Analysis Report Template is far more than an administrative document; it is a foundational pillar of a sound risk management framework. By standardizing the evaluation process, it brings consistency, efficiency, and completeness to what can be a highly complex assessment. The template ensures that every credit decision is supported by a thorough analysis of the 5 Cs of credit, a deep dive into financial statements, and a clear-eyed view of both quantitative and qualitative risks.

For any organization that extends credit, investing the time to develop and implement a robust template is a strategic imperative. It empowers analysts to make more informed and objective decisions, reduces the likelihood of costly defaults, and creates a transparent and auditable record of the credit review process. Ultimately, a great template transforms raw data into actionable intelligence, enabling businesses and financial institutions to lend confidently and grow sustainably.

]]>