Navigating the world of finance requires clear, transparent, and ethically sound documentation. For individuals and businesses seeking Shariah-compliant financing, a well-structured Islamic Loan Agreement Template is not just a formality but a foundational document that ensures the entire transaction aligns with the principles of Islamic law. Unlike conventional loan documents that are centered around the concept of interest, an Islamic agreement is built upon principles of trade, partnership, and risk-sharing, reflecting a fundamentally different approach to lending and borrowing. This guide will delve into the intricacies of these agreements, providing a comprehensive overview for anyone looking to engage in financial dealings that are both legally robust and spiritually compliant.

The core distinction that shapes every clause in an Islamic financial agreement is the strict prohibition of Riba, which is often translated as interest or usury. In conventional finance, money is treated as a commodity that can be rented out for a price (interest). Islamic principles, however, view money as a medium of exchange, not an asset that can generate more money on its own. Therefore, any profit must be derived from the exchange of real assets or services, or through a partnership where risk and reward are shared. This means that an Islamic loan is not a loan in the conventional sense but rather a financing arrangement structured as a sale, lease, or joint venture.

Understanding this distinction is crucial for appreciating why a standard loan template cannot simply be adapted for Islamic use by replacing the word “interest” with “profit.” The entire mechanical and ethical framework is different. An Islamic agreement must be transparent about the underlying asset, the profit margin (in the case of a sale), or the profit-sharing ratio (in the case of a partnership). This article will break down the essential components, explore the most common types of Islamic financing structures, and offer guidance on what to look for in a template to ensure your financial dealings are grounded in fairness, transparency, and faith.

Understanding the Foundations of Islamic Finance

Before diving into the specifics of an agreement, it is essential to grasp the core principles of Islamic finance that govern these documents. These principles are not merely suggestions but are binding rules derived from the Qur’an and the Sunnah (the practices of Prophet Muhammad, peace be upon him). They ensure that all financial transactions are ethical, just, and contribute to a productive economy.

The most prominent principle is the absolute prohibition of Riba (interest). This means that any predetermined, fixed return on a loan is forbidden. The lender cannot profit simply from the act of lending money; profit must be generated through legitimate trade or investment in a real asset or venture.

Another key principle is the prohibition of Gharar, which refers to excessive uncertainty, ambiguity, or risk in a contract. A contract must have clear and specific terms regarding the subject matter, price, and delivery time. This is why Islamic agreements require a detailed description of the underlying asset being financed, leaving no room for speculation that could lead to disputes.

Finally, Islamic finance prohibits Maysir, which means gambling or speculation. This principle forbids transactions where wealth is created by chance rather than through productive effort. Contracts cannot be based on the outcome of an uncertain event. Instead, financing must be linked to tangible economic activity, ensuring that capital is directed towards productive use rather than speculative ventures. Together, these principles of prohibiting Rida, Gharar, and Maysir create a framework for finance that emphasizes fairness, risk-sharing, and asset-backed transactions.

Key Differences: Islamic vs. Conventional Loan Agreements

While both Islamic and conventional loan agreements serve to formalize a financial transaction, their underlying philosophies and structures are worlds apart. Recognizing these differences is the first step in understanding why a specialized Islamic agreement is necessary.

The Concept of Interest (Riba)

The most fundamental difference lies in the treatment of interest. A conventional loan is a debt-based instrument where the lender provides a sum of money to the borrower, who agrees to repay the principal plus a predetermined amount of interest over time. The lender’s profit is the interest charged. In stark contrast, an Islamic agreement completely forbids Riba. Profit for the financier is generated through other Shariah-compliant mechanisms, such as a mark-up on an asset sale (Murabaha) or rental income from a leased asset (Ijarah).

Risk and Reward Sharing

Conventional lending places the vast majority of the risk on the borrower. The lender is guaranteed a return in the form of interest, regardless of whether the borrower’s venture succeeds or fails. If the borrower defaults, the lender can seize collateral to recover their principal and accrued interest. Islamic finance, on the other hand, promotes a more equitable system of risk-sharing. In partnership models like Musharakah (joint venture), both the financier and the client contribute capital and share in the resulting profits and losses based on pre-agreed ratios. This aligns the interests of both parties, as they both have a stake in the success of the venture.

Asset-Backed vs. Money Lending

A conventional loan is essentially the “renting” of money. The transaction involves lending cash and receiving more cash in return. Islamic finance mandates that transactions must be asset-backed. This means that the financing must be tied to a specific, tangible asset (like a car, a house, or equipment) or a service. The financier doesn’t just lend money; they might purchase an asset and sell it to the client, or lease it to them. This ensures that the financing is directly linked to real economic activity and prevents the creation of debt from pure monetary speculation.

Common Types of Islamic Financing Contracts

An Islamic loan agreement is not a one-size-fits-all document. The structure of the agreement depends entirely on the type of Islamic financing contract being used. Each contract type has a unique mechanism for generating profit in a Shariah-compliant manner.

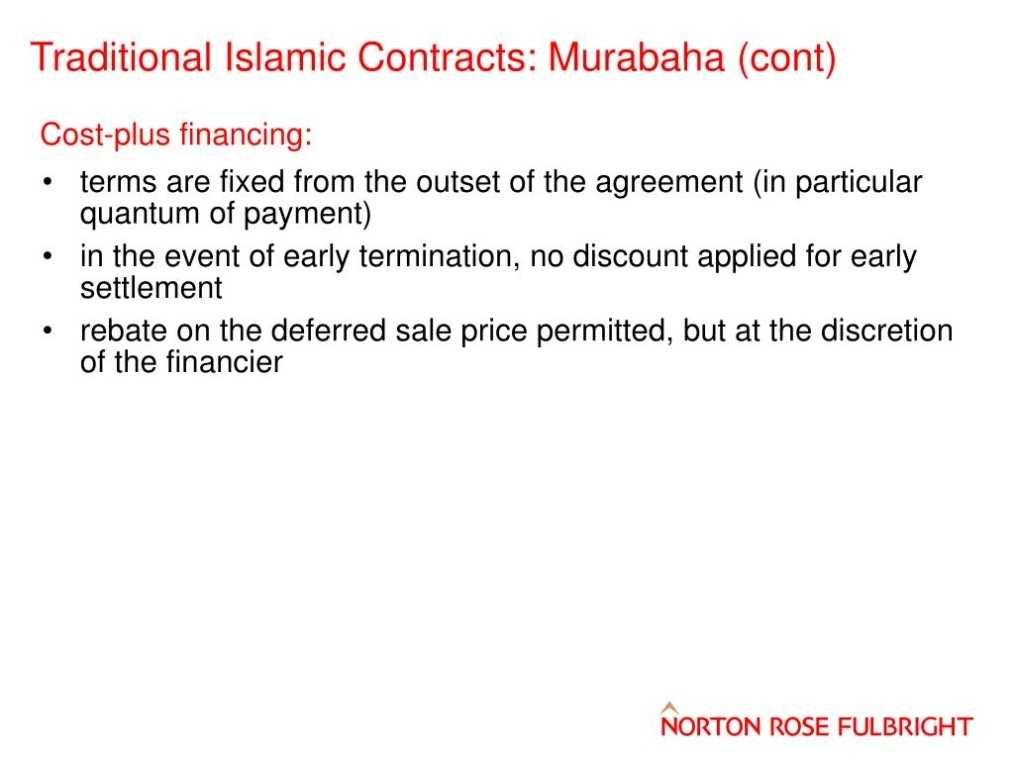

Murabaha (Cost-Plus Financing)

Murabaha is one of the most common forms of Islamic financing, especially for asset acquisition. In this model, the client identifies an asset they wish to purchase. The financier then buys the asset directly from the vendor and subsequently sells it to the client at a marked-up price. The client pays this new price in installments over an agreed period. The key here is transparency: the original cost of the asset and the financier’s profit margin (the mark-up) are known and agreed upon by both parties from the outset. The agreement will clearly state these figures, the payment schedule, and the terms of the sale.

Ijarah (Leasing)

Ijarah is the Islamic equivalent of a lease. The financier purchases an asset (e.g., a car or equipment) and leases it to the client for a specified term in exchange for rental payments. The Ijarah agreement will detail the rental amount, payment frequency, and the duration of the lease. A common variation is Ijarah wa Iqtina (lease and purchase), where the agreement includes a promise for the financier to transfer ownership of the asset to the client at the end of the lease term, either as a gift or for a nominal price.

Musharakah (Joint Venture/Partnership)

Musharakah is a partnership agreement where two or more parties contribute capital to a business or project. Profits are distributed among the partners according to a pre-agreed ratio, which does not necessarily have to be proportional to their capital contribution. However, losses are strictly shared in proportion to each partner’s capital investment. This is a true risk-sharing model, often used for business financing and real estate investment. The agreement must clearly define the capital contributions, management responsibilities, and the profit-and-loss sharing ratios.

Mudarabah (Profit-Sharing Partnership)

Mudarabah is a partnership where one party, the Rabb-ul-Mal, provides the capital, and the other party, the Mudarib, provides the expertise and manages the venture. Profits are shared between them according to a pre-agreed ratio. In the event of a loss, the entire financial loss is borne by the capital provider (Rabb-ul-Mal), while the manager (Mudarib) loses their time and effort. This model is common in Islamic banking for investment accounts and project financing.

Qard al-Hasan (Benevolent Loan)

A Qard al-Hasan is a truly interest-free loan extended on the basis of goodwill. The borrower is only required to repay the principal amount. While the lender may accept a voluntary, unsolicited “gift” (hiba) from the borrower upon repayment, this cannot be stipulated in the contract. This type of loan is considered a charitable act rather than a commercial transaction and is often used for humanitarian or social purposes. The agreement for a Qard al-Hasan is typically simple, focused solely on the principal amount and the repayment terms.

Essential Clauses in an Islamic Loan Agreement Template

A robust and compliant Islamic Loan Agreement Template must contain specific clauses that reflect the principles of Shariah. These clauses differ significantly from those found in conventional agreements.

Identification of Parties

This is a standard clause in any legal document. It must include the full legal names, addresses, and official identification details of all parties involved, whether they are individuals or business entities. The roles of each party (e.g., Financier/Seller, Client/Buyer, Partner) should be clearly defined.

Description of the Underlying Asset or Venture

This clause is critical for Shariah compliance. It must provide a precise and unambiguous description of the asset being financed. For a Murabaha agreement, this includes details like the make, model, and serial number of a vehicle or the legal description of a property. For a Musharakah agreement, it would detail the nature of the business venture. This specificity helps to eliminate Gharar (uncertainty).

Contract Type Specification

The agreement must explicitly state which Islamic financing structure is being used (e.g., Murabaha, Ijarah, Musharakah). This is crucial because the rights and obligations of the parties are determined by the type of contract. Simply calling it an “Islamic financing agreement” is not sufficient.

Payment Schedule and Amount

This section must clearly outline the financial terms. In a Murabaha agreement, it will specify the original cost of the asset, the financier’s profit margin, the final sale price, the installment amount, due dates, and the total duration of the repayment period. For an Ijarah, it will detail the rental payments. The total amount owed cannot increase over time, as this would constitute Riba.

Terms of Ownership and Transfer

The agreement must be very clear about the ownership (milkīyah) of the asset at each stage of the transaction. For example, in a Murabaha, the financier must take legal possession and ownership of the asset before selling it to the client. In an Ijarah wa Iqtina, the contract must specify the exact conditions under which ownership will be transferred to the lessee at the end of the term.

Default and Late Payment Provisions

Handling late payments is a sensitive area in Islamic finance. Since charging interest on late payments is forbidden, agreements must use alternative, Shariah-compliant methods. A common approach is to include a clause where the client agrees to pay a predetermined penalty amount for late payments, which the financier is then obligated to donate to a designated charity. This serves as a deterrent for the client without benefiting the financier, thus avoiding Riba. This compensation is known as Ta’widh.

Governing Law and Dispute Resolution

This clause specifies the legal jurisdiction that governs the agreement. It may also stipulate that any disputes should be resolved in accordance with Shariah principles, potentially through arbitration by a panel of Shariah scholars or a recognized Islamic dispute resolution body.

Creating Your Agreement: A Step-by-Step Guide

Drafting a Shariah-compliant agreement requires diligence and care. While a template provides a foundation, it often needs to be customized for a specific transaction.

Step 1: Define the Purpose and Nature of the Financing

First, clearly identify what is being financed. Is it a home, a business vehicle, inventory, or start-up capital? The nature of the transaction will heavily influence the most suitable Islamic financing model to use.

Step 2: Choose the Appropriate Shariah-Compliant Structure

Based on the purpose, select the correct contract type. For purchasing a physical item, Murabaha is often ideal. For using an asset over time, Ijarah is more appropriate. For starting a business with a partner, Musharakah is the correct choice. This decision is fundamental to the entire agreement.

Step 3: Draft the Core Clauses

Using a reliable template as a guide, draft all the essential clauses mentioned in the previous section. Pay close attention to detail, especially regarding the description of the asset, the calculation of profit or rent, the payment schedule, and the default provisions. Ensure there is no ambiguity.

Step 4: Seek Professional and Shariah Consultation

This is the most critical step. It is highly inadvisable to finalize a significant financial agreement without professional oversight. You should consult with two key experts: a legal professional familiar with contract law in your jurisdiction, and a qualified Shariah scholar or advisory firm specializing in Islamic finance. The lawyer ensures the contract is legally enforceable, while the Shariah advisor ensures it is compliant with Islamic principles.

Common Pitfalls to Avoid

When structuring an Islamic financial agreement, several common mistakes can render the contract non-compliant or invalid.

Hidden Interest (Riba)

A frequent error is creating a “synthetic” Islamic agreement that mimics the economics of a conventional loan. For example, structuring a Murabaha sale where the financier never actually takes possession of the asset, or where late payment penalties are treated as income for the financier. These are forms of hidden Riba and must be avoided.

Excessive Uncertainty (Gharar)

Contracts with vague terms are non-compliant. For instance, an agreement to finance an “unspecified property” or a business venture with an undefined profit-sharing mechanism would be invalid due to Gharar. All key elements—the asset, price, profit/loss ratios, and timelines—must be explicitly defined.

Lack of a Tangible Asset

Remember, Islamic finance must be tied to the real economy. An agreement that is essentially a loan of cash to be repaid with a premium, without any underlying asset sale or lease, is not a valid Islamic transaction (except for a Qard al-Hasan, which is interest-free).

Using Conventional Templates

Simply taking a conventional loan agreement and replacing the term “interest” with “profit” or “mark-up” is a critical error. The entire structure of the contract, from ownership transfer to risk allocation, is different. Using a conventional template fundamentally misunderstands the principles of Islamic finance and will almost certainly result in a non-compliant agreement.

Conclusion

An Islamic loan agreement is more than just a legal document; it is a testament to conducting financial affairs in a manner that is ethical, just, and aligned with the principles of faith. It moves away from the debt-based, interest-centric model of conventional finance towards a system based on trade, partnership, and shared responsibility. The key to a valid agreement lies in its adherence to the prohibitions of Riba, Gharar, and Maysir, and its foundation in real, asset-backed economic activity.

Understanding the distinct structures like Murabaha, Ijarah, and Musharakah is essential for choosing the right framework for your needs. When drafting or reviewing an Islamic Loan Agreement Template, paying meticulous attention to clauses regarding the underlying asset, payment terms, and Shariah-compliant default provisions is paramount. Ultimately, the guidance of qualified legal and Shariah professionals is indispensable to ensure that your agreement is both legally sound and spiritually pure, providing a solid foundation for a fair and transparent financial relationship.

]]>